Robust Work/Life Benefits

In addition to offering covered employees and their family members professional EAP counseling and coaching support, Employee Assistance of the Pacific goes farther to provide support for those Life issues that impact your Work.

In addition to offering covered employees and their family members professional EAP counseling and coaching support, Employee Assistance of the Pacific goes farther to provide support for those Life issues that impact your Work.

All you have to do to receive free consultation for Legal issues, Financial issues, or Eldercare/Healthcare Navigation issues, is just give us a call. We'll take your information down and line you up with our legal, financial, or eldercare experts.

Please note that work-related legal issues or financial issues are not covered.

Most of our covered companies provide these service, but not all. So if you have an questions about whether you are eligible to receive these services just give us a call.

COUNSELING

Individual employees and their covered family members can discuss their personal problems with a professional…

LEGAL

Any time you need an attorney, you can call the EAP and we’ll get you a free 30-minute consultation with one of the attorneys in our network…

FINANCIAL

Any time it would help to talk with an independent expert to help you get started in the right direction you can call us…

HEALTHCARE NAVIGATION

Having an expert who can guide you through complex eldercare issues or the healthcare maze is a great timesaver…

MEDIATION

Trained neutral mediators can help you resolve differences in a safe and respectful manner and save you...

IDENTITY THEFT

Fraud resolution specialists can help you recover from an ID theft or fraud-related theft, and get you back on track...

COACHING

Coaching is different from counseling. Your coach can support you, challenge you, and help you find the best way…

FORMS

Our Robust Work/Life Services Help Your Employees Stay Productive!

When we assist your valuable employees with personal issues that trouble them, they become more present, engaged, productive employees.

In addition to providing your employees with counseling, they also have access to a number of Work/Life services that can help them with those issues impacting their work and their lives!

- Healthcare Navigation Consulting

- Financial Consultation

- Legal Consultation

- Identity Theft

- Mediation

Employee Assistance of the Pacific offers Eldercare and Healthcare Navigation Services through Ho’okele Personal Health Navigation, LLC to most covered employees and their families. The eldercare and healthcare system can be a maze and the Ho'okele professionals can help individuals and their families with education, consultation, and referrals. It takes a village to manage a health care crisis or to help a senior to remain independent and safe in their residence as long as possible. Services include but are not limited to understanding a new diagnosis, researching insurance coverage or finding a specialist, a day care program or retirement community. When needed, the navigators can assist with end of life planning and family issues.

In addition to providing you with free counseling through your EAP, most employers also provide you with free Financial Consultation as well.

They understand that any way they can get you started towards financial well-being will ultimately serve you as well as the employer! We can provide a free 30-minute consultation with a financial expert on a variety of topics:

- Budgeting

- Debt Consolidation

- College Financial Planning

- Retirement Planning

- Estate Planning

- Taxes

- Bankruptcy

Call us to arrange for your free Financial Consultation!

Note: Not all employer groups have this benefit. Please call us for availability.

Read MoreIn addition to providing you with counseling, most employers also provide you with free legal consultation through our EAP. They understand that dealing with a legal challenge impacts both your life and your work, and want to help you!

Legal Consultation: A free 30-minute consultation with one of our network attorneys, either face-to-face or by phone, whichever you prefer. You can discuss just about any issue (other than work-related issues) confidentially. If you need additional assistance after the 30 minutes, they will also reduce their ongoing rate by 25% so this can be a tremendous cost savings!

Call us today to see about obtaining a free legal consultation!

Note: Most, but not all corporate customers have this benefit for their employees. Call us for availability.

Read More

If you are ever a victim of Identity Theft, you can call the EAP and we will provide you with a free 60-minute consultation with a Fraud Resolution Counselor.

In the event of an identity theft or fraud-related event, our Fraud Resolution Specialists can help you with seven emergency response activities:

- You can receive a Uniform ID Theft Affidavit and get answers to your questions about how to complete it and where to submit it.

- You can receive fraudulent account forms or letters for itemizing each fraudulent occurrence and advice on where to submit them.

- You can be directed where to report the fraudulent activity and how to notify the local and federal authorities, as well as your creditors' fraud departments.

- You can obtain the contact information for the three major Credit Reporting Agencies, and advice on how to obtain a free copy of your credit report now.

- You can receive information on how to place a "Fraud Alert" and/or "Security/Credit Freeze" on your credit file.

- You can receive an ID Theft Emergency Response Kit including contact information and preventative steps to take immediately.

- You can be informed and educated about how ID Theft occurs and informed about protective measures to take to avoid further ID Theft occurences and resulting damage to your credit history and credit score.

Call us today to see about obtaining a free Identity Theft consultation!

Note: Most, but not all corporate customers have this benefit for their employees. Call us for availability. For most covered employees, one hour of Identity Theft Consultation may be exchanged for one hour of your counseling benefit.

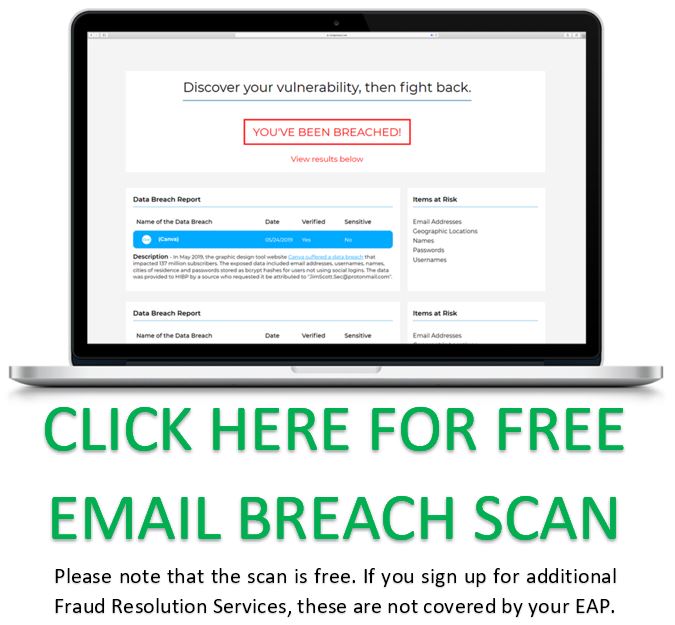

Free Email Breach Scan

The link on the right allows you to enter an email address to scan for potential vulnerability. You can see if your personal or work email addresses have been breached. This scan will also verify what personal information may have been connected with the breach. You can check multiple email addresses for compromised data.

If you need additional support to prevent identity theft before it strikes, employees covered by EAP can purchase Premium Protection for 25% off. These services include 24/7 credit and identity theft monitoring, theft insurance, credit reports and scores, and alert notifications.

If you need additional support to prevent identity theft before it strikes, employees covered by EAP can purchase Premium Protection for 25% off. These services include 24/7 credit and identity theft monitoring, theft insurance, credit reports and scores, and alert notifications.

[Please note that these additional services are not covered by your EAP and only provided as a discounted option for those who may be interested in these services.]

Click for our ID Theft Introductory Webinar (Nov. 2020)

Read MoreOne of the newest additional services we're most excited about in 2021 is our new Mediation benefit.

We have partnered with all five Hawaii Mediation Centers to provide our covered employees with a free 30-minute Intake Session to explore the benefits of Mediation for your situation.

Mediation is a confidential, informal process where a neutral third party (the mediator) can help parties in conflict:

- Talk through your differences,

- Explore and negotiate options in a safe environment,

- Decide how to resolve their dispute, and

- Craft an agreement you both can live with that is fair, realistic, and durable.

Mediation services are voluntary and require all parties to negotiate in good faith. If one party does not want to participate, the mediation cannot occur.

Mediation services are voluntary and require all parties to negotiate in good faith. If one party does not want to participate, the mediation cannot occur.

Trained mediators make sure the process is safe and respectful for all involved.

No paperwork or documentation is provided unless all parties agree.

Mediators cannot be subpoenaed or required to testify in court; nor can any paperwork or records be used in court unless it is a document all parties agree to and sign.

The most commonly mediated issues are:

- Domestic Issues (Divorce agreements and Child custody/visitation/parenting plans)

- Landlord/Tenant Issues

- Condominium and Real Estate

- Consumer / Merchant Issues

- Family and Friend Struggles

- Co-worker Issues

- Neighbor and Pet Issues

- And many others

We have partnered with all five non-profit Mediation Centers across Hawaii:

The Mediation Center of the Pacific (Oahu)

The Mediation Center of the Pacific (Oahu)

Maui Mediation Center

Ku'ikahi Mediation Center (East Hawaii)

West Hawaii Mediation Center

Kauai Economic Opportunity Mediation Program

If you decide after your initial free Mediation Intake Session that mediation would work for you, all five non-profit Mediation Centers offer low cost services.

If you decide after your initial free Mediation Intake Session that mediation would work for you, all five non-profit Mediation Centers offer low cost services.

Successful mediation cases can save you thousands of dollars (even tens of thousands of dollars) in attorney fees and court costs!

Call us today to see about obtaining a free Mediation Intake Session!

Note: Most, but not all corporate customers have this benefit for their employees. Call us for availability.

Click the above image to view our 50-minute video overviewing your Mediation benefit.

Read More